I read Chip War at the same time as reading a very different sort of history book: Foundation by Peter Ackroyd. Whereas Chip War takes a deliberately slowed-down, linear approach to covering the logarithmic growth of the global semiconductor industry, Foundation is a beautifully-written, almost psychedelic million-year narrative of Britain and its inhabitants (of which I’m one).

It’s a strange book-pairing perhaps, but it led me to a fundamental question: Why aren’t more British companies participating in the AI chip boom?

After all, computing is a very British topic. It's a montage that typically begins with daguerrotypes of Babbage and Lovelace in the 1830s, followed by black and white photos of Alan Turing and the Enigma machine a century later. We tend to skip a few decades to give people a chance to pop to the loo, before fading back in to colour footage of the 1981 BBC Micro, Acorn Computers and the UK's one truly big commercial success story: ARM, which is now publicly owned with a $250bn market cap (through Nasdaq not the LSE, mind you).

But none of this stuff takes up much space in Chip War, and for good reason.

Chris Miller is an American economic historian and a Russia specialist who zooms in on different decades and different locations to tell a more commercial story: from the development of the transistor at Bell Labs in 1947, through to the first mainstream applications in the 1950s and 60s, supported by US military investment (mainly for chips to be used in missile guidance) during the Cold War, finally culminating in the early 1990s with the rapid growth of US chip companies like Intel, AMD and joined later by NVIDIA (together worth around $7.5 trillion today).

The story then switches to Asia, as American executives went on the hunt for cheaper, non-unionised labour to make their chips. This is one of the best parts of the book, covering how small countries like South Korea and Taiwan, which were even more impoverished after WWII than the UK was, turned potentially superficial and exploitative contracts into long-term domestic wins such as TSMC ($1.9 trillion market cap) and SK Hynix ($1 trillion), not to mention more general electronics companies like Sony and Samsung.

Britain is largely forgotten at this point. But insofar as Chris Miller provides an answer to my initial question, he gives it indirectly: the book repeatedly returns to the theme of risk-taking, and specifically the need for risk-taking by individuals to be matched by government risk-taking through long-term industrial policy commitments that survive political turnover.

One of the individuals covered in the book is Intel’s Andy Grove, born in Hungary as András Gróf, who found in the United States not only safety from the Nazis, but also proactive support for his entrepreneurial drive – including a significant share of the $1bn (in modern dollar value) distributed to Intel and other chip companies by the US Defense Department. Such government help has continued into recent years via grants under the CHIPS Act (some of which have been converted into a shareholding in Intel, as I’ve covered here.)

Miller points out clear parallels with the journey of Morris Chang, who fled China as a child during the Japanese invasion, studied in the US and eventually settled in Taiwan. Like Grove, the uncertainties Chang experienced as a refugee may have fostered his ability to cope with risk. But what really mattered after that was the support of the Taiwanese government, which effectively became Chang’s anchor investor when he pitched the idea of building TSMC.

Contrast these examples against the story of Inmos – a British company that is understandably not covered at all in Chip War. It was founded with the equivalent of around $300m of public money in the 1970s – a significant sum – and built a chip fabrication plant in Wales. It was then abandoned when Margaret Thatcher came to power, and ultimately folded into what is now the Swiss-Dutch company STMicroelectronics, whose share price has surged 170% in the past six months (a statistic I mention in a "look what you could have won" sort of way).

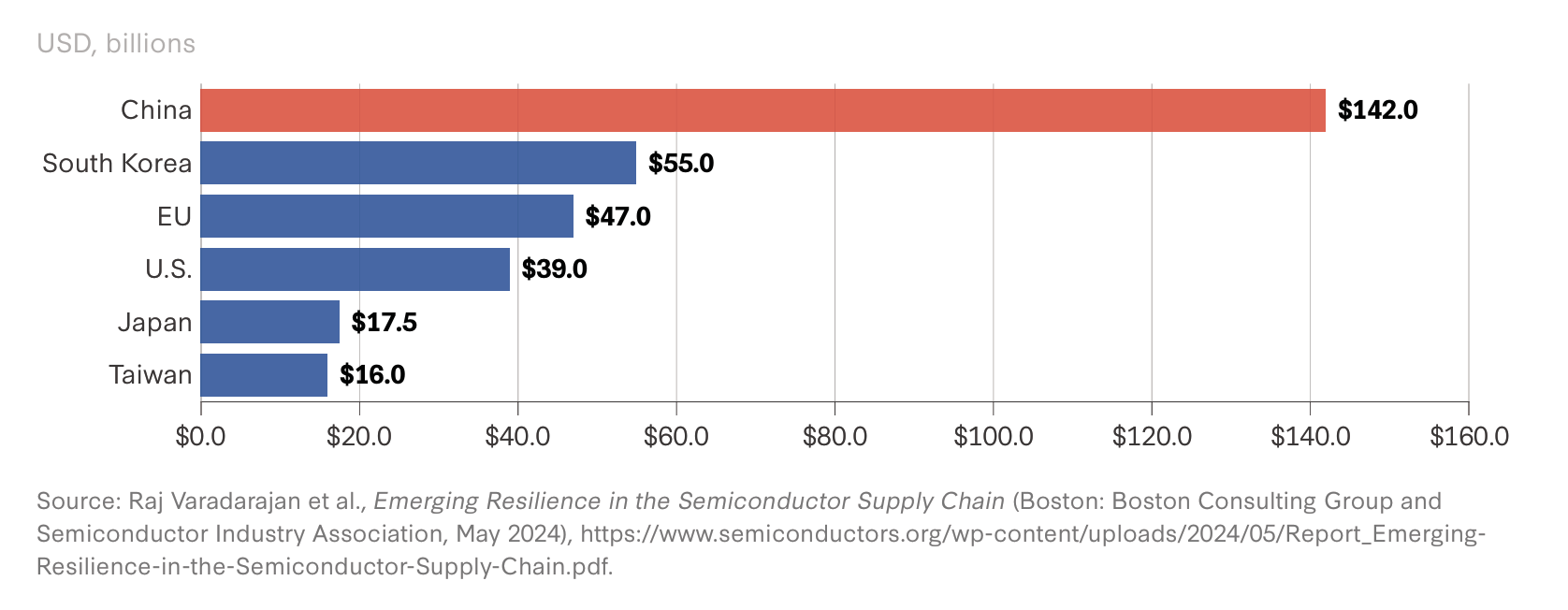

Committed British support for its homegrown chip industry is today barely worth $1.3bn spread over a decade. This is orders of magnitude lower than what others have been spending, as shown in the CSIS chart above, which is based on BCG and SIA data. Even when you look at spend per capita, the gap is enormous: $18 in the UK versus over $100 in the US, EU and China.

This is hardly a recipe for change. If anything, the data should point investor attention more towards the EU than to the UK. However, returning to Ackroyd’s Foundation, which I’d recommend to anyone who's interested in island stories, I wouldn’t be too disparaging about the UK’s technological future, especially with major geopolitical schisms looming elsewhere. What the country has evidently lacked in sustained political will and industrial spending, it might make up for with other, deeper sorts of continuity – not least the sort of legal, linguistic and intellectual openness that produced Lovelace and Turing in the first place.