Stan Shih’s smile curve is a decades-old concept, but it’s still relevant to investors who have been watching Intel’s share price (INTC, up 100% in the first four months of 2026).

Shih’s theory, which has since been observed across multiple industries and geographies, holds that more value in manufacturing tends to accrue to IP- and brand-owning companies at the edges of the value chain, than to pure fabricators in the centre.

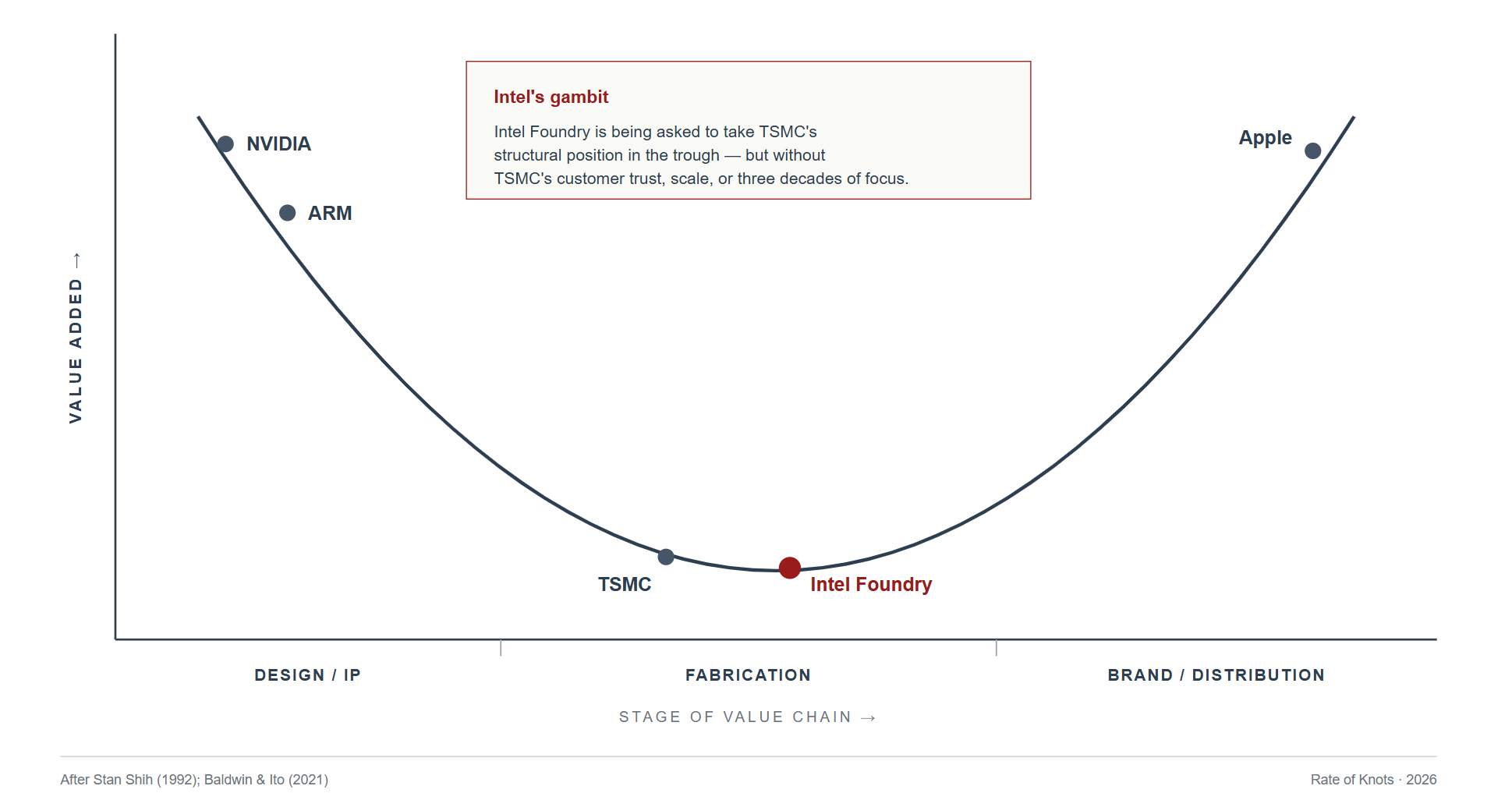

Applying this idea to the semiconductor industry, you expect to find valuable design companies like NVIDIA and ARM at one end of the smile and consumer-centric giants like Apple at the other.

In the middle of the trough sits TSMC.

Is the market hoping Intel will join it? If so, that’s a tough journey with an even tougher destination.

As the world’s dominant chip fabricator and one of the most successful manufacturers of all time, TSMC is continually forced to take on the risk of huge capex investment (expected to exceed $52bn in 2026, more than 3x Intel’s planned spend). This investment is funded by profit margins that are 20+ points worse than those of its fabless customers (one extreme metric to illustrate this: TSMC shareholders end up with a 40% return on equity, versus NVIDIA’s 115%). To survive the infamous cyclicality of its industry, TSMC must also maintain a war chest of over $25bn in idle cash, equivalent to half a year of capex that cannot be put to work.

Geostrategically, this all makes sense. That’s why Taiwan props up TSMC and why the US has more recently subsidised Intel. The Trump administration’s conversion of that subsidy into a $9bn equity stake was a smart decision not because that holding is now worth $36bn on paper, but because it gives American industry a shot at an AI future that is less at risk from China.

Commercially, however, the rationale for Intel trying to emulate TSMC is less clear. TSMC has always been careful never to compete with its own customers. Intel can’t make that promise. Instead, it’s building a plausible firewall between its “Product” and “Foundry” subsidiaries, to the point of having separate ERP systems (by end of 2027) and giving its Product arm the freedom to use TSMC chips if it wishes. But even if customers like NVIDIA or AMD are ready to trust the firewall with their IP, they’re not likely to give a competitor extra cash flow unless it’s absolutely necessary.

For this reason and others, analysts have envisioned a full spin out of Intel Foundry, similar to how AMD spun out GlobalFoundries. But the US government has already positioned itself to block this. The Treasury's warrants effectively veto any sale of more than 50% of the foundry, which means the structural fix that would unlock customer trust is also the one Intel can no longer take.

This is perhaps the biggest long-term risk that Intel investors must face: misaligned interests with their co-shareholder, the US government. Investors seem to regard government involvement as a net positive and perhaps even a price floor, whereas it could just as easily be a blocker to strategic agility and growth.

Ultimately, this could result in the US CHIPS Act facilitating a transfer of wealth from US taxpayers, through Intel, to the fabless designers who ultimately capture the rents from bleeding-edge silicon. That might be a defensible policy outcome in a world at serious risk from US-China schism, but it’s not an investment thesis.

Recommended Reading:

The Globotics Upheaval: Globalisation, Robotics and the Future of Work – written by Richard Baldwin, who happens to be a recent exponent of the smile curve theory.

Chip War, by Chris Miller – more history than analysis, but helps to make sense of the industry as a whole.

Power and Prediction: The Disruptive Economics of Artificial Intelligence, by Agrawal, Gans and Goldfarb - a more general look at where AI is likely to cause value to accrue, beyond the usual suspects.

Disclaimer: Published for informational and educational purposes only. Nothing here constitutes investment advice, a recommendation, or a solicitation to buy or sell any asset. I invest only my own capital, with a focus on AI and semiconductors, and may hold positions in assets discussed — only ever as a small part of a broadly diversified portfolio.