A short review of Our Dollar, Your Problem (2025)

I listened to Rogoff being interviewed when his book launched last year and decided it was worth going straight to the source. I particularly wanted to understand the so-called "convenience premium" that podcasters kept asking him about. (In a nutshell, that's the estimated $120bn bonus the US government gets every year as a result of being able to borrow at a lower interest rate than other governments, because its dollar debt is so darned convenient for lenders to hold or use as collateral.)

As it turned out, the convenience premium was the least interesting part of the book. The richest material is in the first half, when Rogoff risks wandering off topic to give us journal-like impressions of his global travels as an international chess player, academic and eventually as chief economist of the IMF. Three of those digressions were especially useful to my under-construction understanding of chokepoints in the global financial system — particularly the role of non-state money (Bitcoin), modern political currencies like the euro, and supranational institutions like the IMF.

1. Bitcoin has accumulated intrinsic value for reasons that aren't fully appreciated

Rogoff is no crypto evangelist, but he has a refreshingly pragmatic view of Bitcoin. His early travels as a chess player gave him a sharp ear for what he calls the "underground economy" — the cash-and-quiet transactions that have sat outside formal banking. For decades that economy ran on hundred-dollar bills. It now runs increasingly on Tether, USDC, and Bitcoin – with Bitcoin being the option that is least susceptible to weaponisation risks that affect dollar stablecoins and the dollar itself. For Rogoff, that's enough to argue crypto is not "going to zero", the way so many other commentators assume, even as he warns that its unregulated status makes it ripe for crises.

Where I part company with Rogoff is on what a crypto crisis would actually do to Bitcoin specifically. He treats "crypto" as a single category, but a run on USDC or USDT — possibly triggered by fears about their traditional financial collateral or the chain of institutions underwriting them — would likely increase Bitcoin's price, not decrease it. Stablecoin holders rushing to preserve wealth would move into Bitcoin via decentralised exchanges, which is exactly the asset's failure-mode value proposition.

2. The euro is the most underrated success story in modern monetary history

Rogoff readily admits he expected the euro to fail, and to fail miserably. Instead, against the institutional incoherence of the eurozone and a generation of crises, it has become the world's second currency and the only fiat currency with any plausible claim to challenge the dollar – and this has been achieved through the sustained force of political will. Despite all the debate in the UK about Brexit and European integration, I've remained largely oblivious to the scale of this achievement.

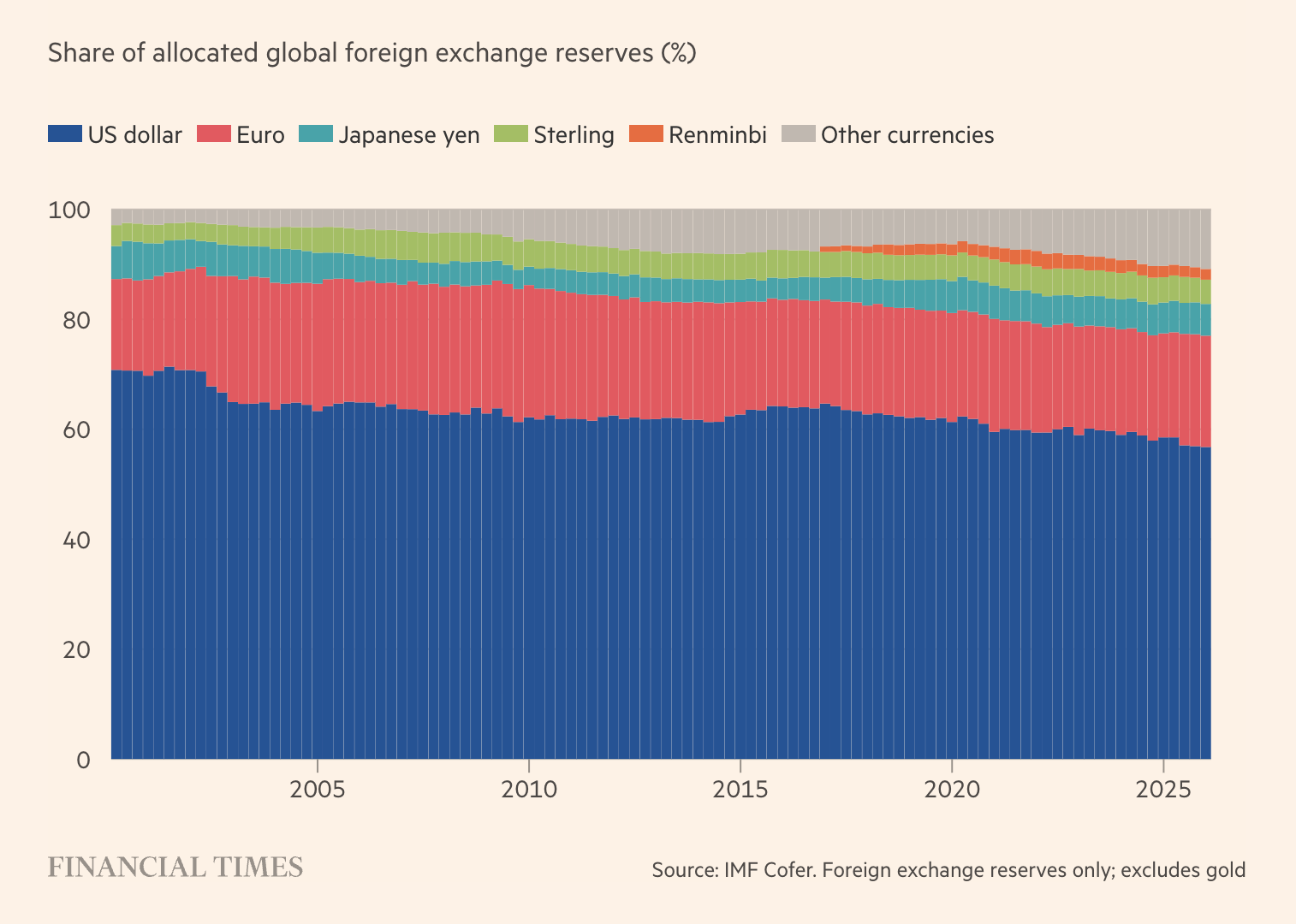

The chart above shows there's little sign of the euro gaining ground against the dollar right now. Nevertheless, reading Rogoff's chapters made me more determined to maintain some euro exposure in my own savings, not only because I might want work and live on the "mainland" in the future (I spent some blissful years in Bordeaux during Covid and would love to go back there), but also because I think it's a smart diversification in principle, just in case GBP continues to tank. (In the early days of the euro, you could get 1.5 of them to the pound – now you get only 1.15.)

3. The IMF explains why the US still bothers with multilateralism

With the US exiting so many international treaties and agreements, it has struck me as a conundrum that it has remained so active and committed within the International Monetary Fund. Reading Rogoff's book, it dawned on me that I had very little idea of how the IMF really worked.

This is what I learned: The IMF runs on an internal reserve asset called the Special Drawing Right (SDR), which lets selected crisis-borrowers access something close to rich-country interest rates. It is the rich countries that decide which poor countries get IMF support and which don't, which makes sense since its the rich countries offering the help. Except, IMF lenders like the US aren't actually putting their own wealth at risk in making these loans, so much as sharing limited access to their own borrowing rates, which are of course cheap thanks to the convenience premium mentioned earlier. Rogoff's insider explanation makes it clear that the IMF remains a relatively low-cost, high-leverage extension of dollar power. Defunding it would cost the US far more influence than it would save in dues. Rogoff makes it clear that he doesn't even like the IMF's lending mechanism and would rather just see rescue packages given as aid – which really says it all.